Another Homeowner Disputes South's Earthquake Insurance Policy

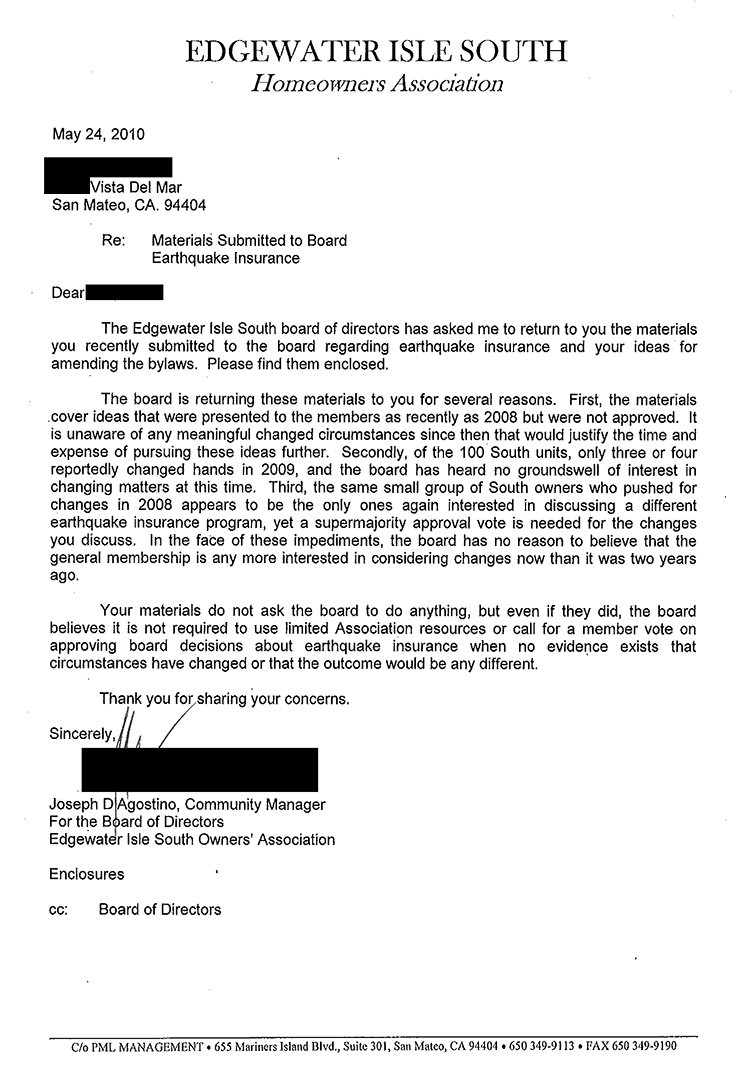

June 7, 2010

Three years after one homeowner's campaign to dump the Edgewater Isle South Associations' earthquake insurance coverage, another homeowner has again come forward with similar, yet more detailed, concerns. This time, the homeowner has explained in excruciating detail why this is a bad policy, beyond the concern of how much it is raising homeowners' dues.

The Edgewater Isle South Owners Association SHOULD HAVE called a special meeting to discuss and vote on this issue, but of course, 2 months later, they have not.

UPDATE: July 6, 2010

The board of directors has solely determined that they will not let the homeowners vote on this measure. (See bottom of page.)

April 7, 2010

To: Edgewater Isle South Homeowners

Re: Edgewater Isle South HOA Earthquake Insurance

Dear Neighbor,

I recently presented to the Edgewater Isle South Board of Directors a petition that was signed by nine homeowners to allow homeowners to vote on earthquake insurance. I have attached the following information to help homeowners better understand this issue:

1. Our coverage at a glance, this gives you a snapshot of our current earthquake insurance coverage.

2. Information about our current coverage and possible solutions.

3. California D-1 form, this is a disclosure that an insurance company must give to those who purchase a non-admitted policy (this is the status of our current policy).

The annual premium for the earthquake policy has trended at over 100k for the last three years (over $1000 per homeowner). While the premium is an issue, the bigger issue is the coverage. While getting coverage is well intended as we do face earthquake risks to our buildings, my research tells me that the policy probably won't do much for us, if anything at all.

If you have any questions or if you feel I am incorrect on anything, I always welcome your response, this includes board members. I also encourage you to attend the upcoming annual meeting on April 19th as well as support giving the homeowners the right to vote on earthquake insurance.

Joseph

Information every Edgewater Isle South Homeowner should know

Earthquake Insurance options for Edgewater Isle South does not make sense, here is why:

☑ Coverage is through a non-admitted (non-Licensed) company, this means if we have a dispute with the insurance company in the event of a claim, we would have to take legal action, costing us even more.

☑ The policy has exclusions, during a claim, the insurance company will not cover anything that is excluded because it's part ofthe contract. One example of an exclusion is that our foundation is not covered .

☑ The cost is huge, it has run about $1000 to $1200 per unit per year has been the approximate range during the last few years (about 100K to 120k or more per year for the entire association)

☑ The deductible is 20% of our replacement value, it comes out to about $600,000 for a 10 unit building, this is the amount we would have to collectively come up with per building before any coverage is applicable. If damages are below our deductible, we would have no coverage. Our combined deductible is about 6 million.

☑ The pro-rata coverage per homeowner is 50,000 and this coverage would only apply after our huge deductible, it's not a lot of coverage to be paying serious money for.

☑ Our property values are greatly effected by our high HOA dues, $100 more a month per unit make a big difference when people consider purchasing a property in this economy

There are better solutions:

☑ Individual Condo Unit Owners Policies offer an Earthquake option, the cost is about $300 to $700 per year, you can get better coverage by securing coverage on your own, with a deductible of $7,500 (vs. pro-rate $45,000). State Farm, Farmers, Allstate, Safeco, CSAA (AAA) all offer these options through the California Earthquake Authority. These are admitted licensed companies, unlike the non-admitted policy the HOA carries. For more info, please see http://www.earthquakeauthority.com/

☑ A number of other earthquake only insurance companies offer various options, you want to visit http://www.eqins.com

☑ Some homeowners may want to take this risk on their own and have the reserves to pay for earthquake on their own (it's an unpleasant expense, but a reality we face by living in the Bay Area), this should be each homeowner's choice .

☑ Some may want to choose a combination of the above. We all have different finances, giving the power back to the homeowner allows each to make a decision that is best fit for our own financial situation.

Additional items to keep in mind:

☑ The board can still get an earthquake policy under the proposed changes, all they need is provided the details of the policy and a majority of the vote.

☑ This will not only save us a huge amount on dues, it will increase our property values, something we really need in this real estate market.

☑ Previous earthquakes have proven that older buildings sustain damage (pre-1970), but newer building hold up better. In addition to our building being built in 1986, it has been retrofitted and strengthened to help prevent or minimize earthquake damage.

☑ 93% of all damage in the 1994 Northridge Earthquake were partially damaged (vs. total destruction), of those insured, many were not covered because they fell below the deductible.

Please support giving homeowner the right to vote on earthquake insurance coverage, this is a decision that financially impacts all of us.

NOTICE:

1. THE INSURANCE POLICY THAT YOU ARE APPLYING TO PURCHASE IS BEING ISSUED BY AN INSURER THAT IS NOT LICENSED BY THE STATE OF CALIFORNIA. THESE COMPANIES ARE CALLED "NONADMITTED" OR "SURPLUS LINE" INSURERS.

2. THE INSURER IS NOT SUBJECT TO THE FINANCIAL SOLVENCY REGULATION AND ENFORCEMENT WHICH APPLIES TO CALIFORNIA LICENSED INSURERS.

3. THE INSURER DOES NOT PARTICIPATE IN ANY OF THE INSURANCE GUARANTEE FUNDS CREATED BY CALIFORNIA LAW. THEREFORE, THESE FUNDS WILL NOT PAY YOUR CLAIMS OR PROTECT YOUR ASSETS IF THE INSURER BECOMES INSOLVENT AND IS UNABLE TO MAKE PAYMENTS AS PROMISED.

4. CALIFORNIA MAINTAINS A LIST OF ELIGIBLE SURPLUS LINE INSURERS APPROVED BY THE INSURANCE COMMISSIONER. ASK YOUR AGENT OR BROKER IF THE INSURER IS ON THAT LIST, OR VIEW THAT LIST AT THE WEB SITE OF THE CALIFORNIA DEPARTMENT OF INSURANCE: WWW.INSURANCE.CA.GOV.

5. FOR ADDITIONAL INFORMATION ABOUT THE INSURER YOU SHOULD ASK QUESTIONS OF YOUR INSURANCE AGENT, BROKER, OR "SURPLUS LINE" BROKER OR CONTACT THE CALIFORNIA DEPARTMENT OF INSURANCE, AT THE FOLLOWING TOLL-FREE TELEPHONE NUMBER: 1-800-927-4357.

6. IF YOU, AS THE APPLICANT, REQUIRED THAT THE INSURANCE POLICY YOU HAVE PURCHASED BE BOUND IMMEDIATELY, EITHER BECAUSE EXISTING COVERAGE WAS GOING TO LAPSE WITHIN TWO BUSINESS DAYS OR BECAUSE YOU WERE REQUIRED TO HAVE COVERAGE WITHIN T'~O BUSINESS DAYS, AND YOU DID NOT RECEIVE THIS DISCLOSURE FORM AND A REQUEST FOR YOUR SIGNATURE UNTIL AFTER COVERAGE BECAME EFFECTIVE, YOU HAVE THE RIGHT TO CANCEL THIS POLICY WITHIN FIVE DAYS OF RECEIVING THIS DISCLOSURE. IF YOU CANCEL COVERAGE, THE PREMIUM WILL BE PRORATED AND ANY BROKER FEE CHARGED FOR THIS INSURANCE WILL BE RETURNED TO YOU."

Date: _________ Insured: _________

SF 198230.2 73670 00741 D-l (Effective January 1,2008)

Board Sits On Petition, Waits Until After Annual Meeting

Edgewater Isle South board of directors waited 2 months to take any "action" (which was none) on this petition. They waited until after the Annual Meeting, which would not have cost them any additional out-of-pocket costs and was the ideal time to take a vote. An annual meeting of members. What a concept.

Now, 2 months later, and after the annual meeting (how convenient), the board has determined that they will not let the homeowners vote on this issue. The board of directors seems to believe it can predict how homeowners would vote. What GALL!

What study did you do to determine there was no new "evidence" that members supported this? Do you just make stuff up as you go along?

The board members resonsible for this fiasco are:

- Jane Fraser

- Lynn Hanlon

- Barbara Finnegan

- Sylvia Morrison

- Jim Newell

What gall you have. Shame on you!

Association Loses Two Small Claims Cases

After all this effort into thwarting the homeowners who wanted to hold a vote, two homeowners sued the Association in small claims court for failure to call a vote. The Association used their trademark sneakiness to then call a vote 28 days before the small claims case. One may conclude they were attempting to influence the outcome of the small claims cases.

Regardless, the Association LOST BOTH small claims cases.

Contact

Contact